This article has been provided by Satis Wealth Management, a sister company of Hillier Hopkins.

The late Jack Bogle – the founder of Vanguard left us all with a simple mantra that he repeated almost every time he wrote an article or gave an interview ‘costs matter’. He also often used to say, ‘in investing you get what you don’t pay for’. And therein lies the rub. In day-to-day life, we tend to make a connection – largely correctly – that you get what you pay for. If you need a good lawyer, it will probably cost you. If you need an accountant to do your tax return, it will cost you.

Yet when it comes to investing the exact opposite applies. The more you pay in ongoing charges to invest in a fund and on all the costs associated with owning the fund over time, means on average, that there is less money left to put in your pocket. It would be easy to select a good fund if all you had to do was pick the most expensive manager, which may cost more than 1% a year. Yet we know, for example, that over 85% of all US equity funds failed to beat the market over 20 years, not least because of the high costs they incur[1]. Trying to pick – in advance – skilled managers who will beat the market in the next 20 years is extremely taxing.

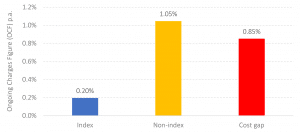

In fact, if you reverse your strategy and pick the cheapest fund, it is likely (although never guaranteed) to be a better option. Taking equity funds available for sale in the UK[2] – both index funds delivering the market return (295 in all), and non-index funds (4,969) seeking to beat the market return, the average costs and the difference between them are set out below.

Figure 1: Equity funds for sale in the UK – Ongoing Charges Figure (OCF)

Source: Morningstar Direct © All rights reserved. Data as at 30th June 2021.

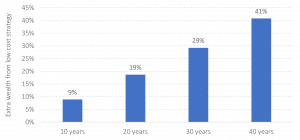

If we assume that both sets of managers (index and non-index) capture the same market returns before costs – a reasonable position to take, in aggregate, as winners and losers have to net out to zero – we can calculate the differential wealth outcomes over time between the less costly index funds and the more costly non-index funds. The seemingly small difference of 0.85% make a huge difference to what an investor’s retirement might look like. The chart below shows you how much more money you would have with the lower cost strategy over different time frames[3].

Figure 2: Wealth outcomes differ depending on costs – lower = generally better

Source: Albion Strategic Consulting using Professor William Sharpe’s Terminal Wealth Ratio calculation.

Put another way, at the end of 40 years – not an unreasonable investing horizon – if the high-cost strategy ended up with £1 million, the lower cost strategy would have £410,000 more to spend, all else equal.

Satis are supporting financial planning week by offering an hour complimentary consultation to discuss your finances. If you would like to book a session click the button below or to visit their website click here.

[1] US Scorecard 2021. https://www.spglobal.com

[2] As of 30th June 2021. Open-ended, UK domiciled funds and ETF, or funds with UK reporting status, publishing KIID OCF

[3] This uses Nobel Laureate William Sharpe’s Total Wealth Ratio calculation